What Is a Bridge Loan? Short-Term Financing That Helps Buyers Move Without Waiting

Buying a new home while still owning your current one puts many buyers in a tough position. You may be financially qualified on paper, but your cash is tied up in equity that you can’t access yet. When timing doesn’t cooperate, a bridge loan can be the tool that keeps your plans moving forward instead of on hold.

A bridge loan is not a one-size-fits-all solution, but for the right buyer in the right situation, it can remove one of the biggest obstacles in a competitive housing market.

The simple explanation of a bridge loan

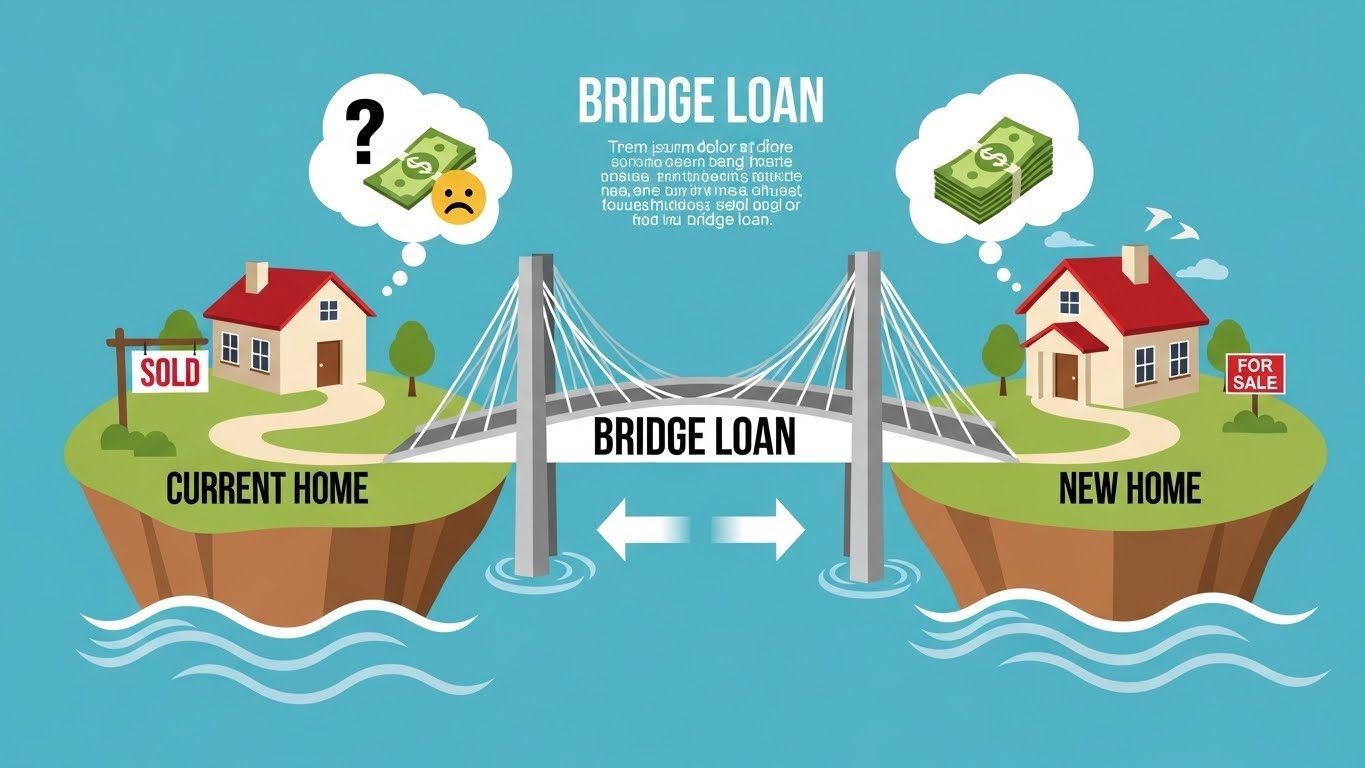

A bridge loan is a temporary loan designed to cover the gap between two real estate transactions. It allows a homeowner to access equity from their current property before it sells, usually to help fund the purchase of a new home.

Instead of waiting for your existing house to close before moving forward, the bridge loan gives you short-term access to cash so both transactions can overlap smoothly.

When buyers typically use bridge loans

Bridge loans are most commonly used when timing creates pressure.

This often happens when:

You find a home you want to buy before your current home sells

Sellers expect non-contingent offers

You need funds for a down payment immediately

You want to avoid temporary housing or double moves

In fast-moving markets, waiting can mean losing the home altogether. Bridge financing is designed to solve that problem.

How bridge loans are structured

Bridge loans are intentionally short-term. Most last anywhere from a few months up to one year. The expectation is that the loan will be repaid once the original property sells.

Key characteristics usually include:

Higher interest rates than traditional mortgages

Short repayment timelines

Interest-only or deferred payment options

Collateral secured by your existing home

Because lenders are taking on additional risk, terms are tighter than conventional loans.

How the process usually works

The lender evaluates the value of your current home and how much equity you have available. Based on that, they approve a loan amount that can be used toward your next purchase.

During the loan period:

You may make interest-only payments, or

Payments may be deferred until your home sells

Once your existing property closes, the bridge loan is paid off using the sale proceeds.

Why bridge loans can strengthen your offer

One of the biggest advantages of a bridge loan is leverage.

When buyers can remove a home-sale contingency, their offers become far more attractive to sellers. In multiple-offer situations, certainty often matters more than price.

A bridge loan allows you to:

Compete with buyers who already sold

Close on your timeline

Negotiate from a position of strength

That flexibility can make a real difference in competitive markets.

What lenders look for before approving a bridge loan

Not everyone qualifies for bridge financing. Lenders typically look for:

Strong equity in your current home

Solid credit history

Verifiable income

The ability to carry overlapping housing costs

Some lenders also want proof that your home is actively listed or market-ready.

Risks and costs to consider carefully

Bridge loans are powerful, but they are not low-risk.

Potential downsides include:

Higher interest rates and fees

Carrying multiple housing obligations

Pressure if your home takes longer to sell

Limited flexibility if market conditions change

If your current home does not sell as expected, the financial strain can increase quickly.

Alternatives worth exploring

Depending on your situation, other options may provide similar flexibility with less risk.

Alternatives can include:

Home equity loans

HELOCs

Cash-out refinancing

Asset-based lending programs

Each option comes with its own trade-offs, and the best solution depends on timing, equity, and risk tolerance.

Is a bridge loan right for you?

Bridge loans work best for financially stable buyers with strong equity and realistic expectations about their home’s sale timeline. They are tools for transition, not long-term solutions.

Before committing, it’s critical to understand the full financial picture and have a backup plan if timelines shift.

Final thoughts

A bridge loan can turn a stressful buying window into a manageable transition, but only when used strategically. The key is knowing when it helps and when it creates unnecessary risk.

If you’re considering buying before selling and want to understand whether a bridge loan makes sense for your situation, professional guidance can save you from costly mistakes.

If you have questions about bridge loans or want help evaluating your options, reach out before making an offer.

📲 Call or text Uriel Resendiz at (818) 940-5530

📧 Email: [email protected]